Award-winning PDF software

ID Form 5305-SIMPLE: What You Should Know

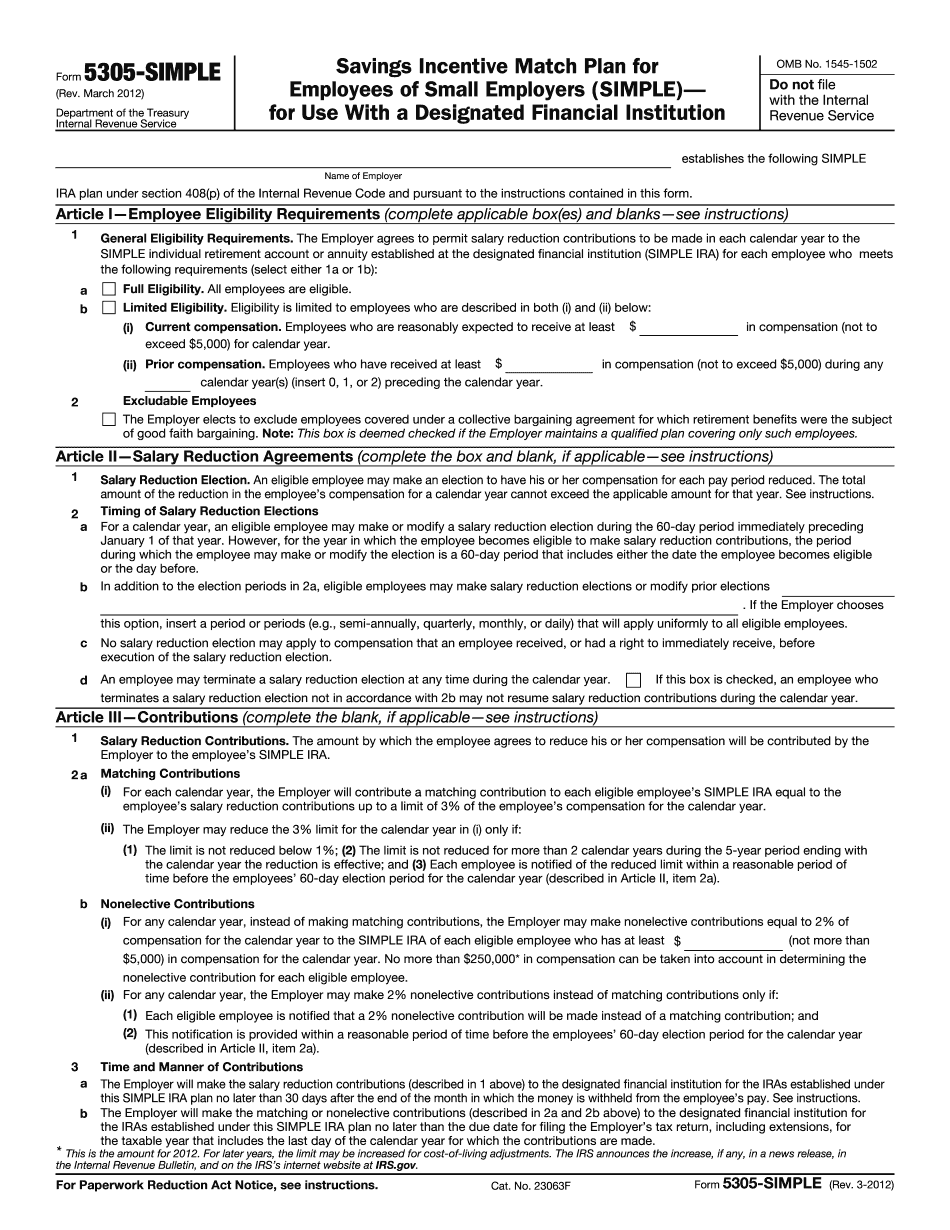

I received a phone call from a client (the National Federation of Independent Business, or FIB, a “business federation” with roughly 2,100,000 employees) who claimed an exception for its members to pay SIMPLE tax by electing to have the SIMPLE IRA distribution tax withheld from their Social Security taxes, but I did not think it was good policy. There was no explanation of that exception, of whether it were allowed, and of the need for some type of special rule to make sure no one who had no other income was taxed for the SIMPLE IRA on the amount of the distribution. It is not reasonable to expect a small business to pay taxes on the amounts of his retirement savings that have been contributed to a SIMPLE IRA. Also, as a financial planner, my experience with the Form 5304 for SIMPLE IRA distribution was that in 90 percent of the cases, the employee did not report income on the Form 5304 and the plan did not withhold tax on the individual's Social Security tax payments. In the last ten percent, I learned that this was not the employee's plan but the employer's plan (which would also not report income), the distribution was tax-free, and the employer had deducted the distributions at source from his employees' Social Security taxes. The employee still had to pay the tax on the Social Security benefits, or on the Social Security equivalent, which is less than the regular amount. I think Form 5304 must be revised to clarify that the employer must continue to withhold tax on the Social Security equivalent of the SIMPLE IRA withdrawal and, in cases where income on the distribution is not reported (and so the plan had no tax withholding at year-end), the employee must still pay tax on the Social Security equivalent of the distribution. Note that employees who participate in a SIMPLE IRA only on a part-time basis should not file a Form 5304 to request comments on the Form 5305 for use with a designated financial institution as an employer because the employer could be in compliance even without the Form 5305 submission. However, if the SIMPLE IRA plan is part of a larger SIMPLE IRA plan that is not a designated financial institution, a Form 5304 is required, even if the Form 5305 would be sufficient.

Online methods assist you to arrange your doc management and supercharge the productiveness within your workflow. Go along with the short guideline to be able to complete ID Form 5305-SIMPLE, keep away from glitches and furnish it inside a timely method:

How to complete a ID Form 5305-SIMPLE?

- On the web site along with the sort, click Commence Now and go to your editor.

- Use the clues to complete the suitable fields.

- Include your personal info and contact data.

- Make certainly that you simply enter right knowledge and numbers in ideal fields.

- Carefully verify the articles from the type in addition as grammar and spelling.

- Refer to aid portion for those who have any queries or tackle our Assistance team.

- Put an digital signature on your ID Form 5305-SIMPLE aided by the enable of Indicator Instrument.

- Once the form is completed, push Finished.

- Distribute the all set variety by means of e-mail or fax, print it out or help save on the product.

PDF editor allows you to make adjustments with your ID Form 5305-SIMPLE from any world-wide-web connected equipment, personalize it in line with your requirements, indication it electronically and distribute in several methods.